For ambitious retail investors looking at the Indian stock market, the question of maximizing returns often leads to a common curiosity: “Can I use borrowed money to buy stocks?” The allure of amplifying your buying power to capitalize on a multi-bagger opportunity is undeniable. However, the Indian financial ecosystem, governed by the Securities and Exchange Board of India (SEBI) and the Reserve Bank of India (RBI), has strict rules in place to protect retail investors from debt traps and to maintain market stability.

- The Short Answer: Yes, But Through Regulated Channels

- Method 1: Margin Trading Facility (MTF)

- Method 2: Loan Against Securities (LAS)

- Method 3: Margin Pledge

- Method 4: Personal Loans – Are They Allowed?

- Pros and Cons of Buying Stocks with Borrowed Money

- The Pros:

- The Cons:

- Transparent Pricing Structure of Paytm Money

- Key Regulatory Guidelines to Remember

- Conclusion

- FAQs

Whether you are looking to take advantage of short-term market fluctuations or simply do not have the immediate cash on hand for a lucrative stock pick, borrowing to invest is a high-risk, high-reward strategy. In this comprehensive guide, we will explore the legal ways you can buy stocks with borrowed money in India, the regulatory guidelines surrounding them, and the critical risks you must consider before taking the plunge.

The Short Answer: Yes, But Through Regulated Channels

Yes, you can buy stocks with borrowed money in India, but you cannot simply walk into a bank, ask for a loan “to buy equity,” and expect an approval. The RBI actively discourages banks from issuing unsecured loans for speculative purposes, which includes stock market trading. Instead, investors use regulated financial instruments provided by authorized stockbrokers and financial institutions. The two primary methods for doing this are the Margin Trading Facility (MTF) and Loan Against Securities (LAS).

Unsecured Loan: A loan that doesn’t require any type of collateral (like a house or car) to be approved.

Speculative Purposes: Financial transactions that carry a high risk of losing value but also hold the expectation of a significant gain.

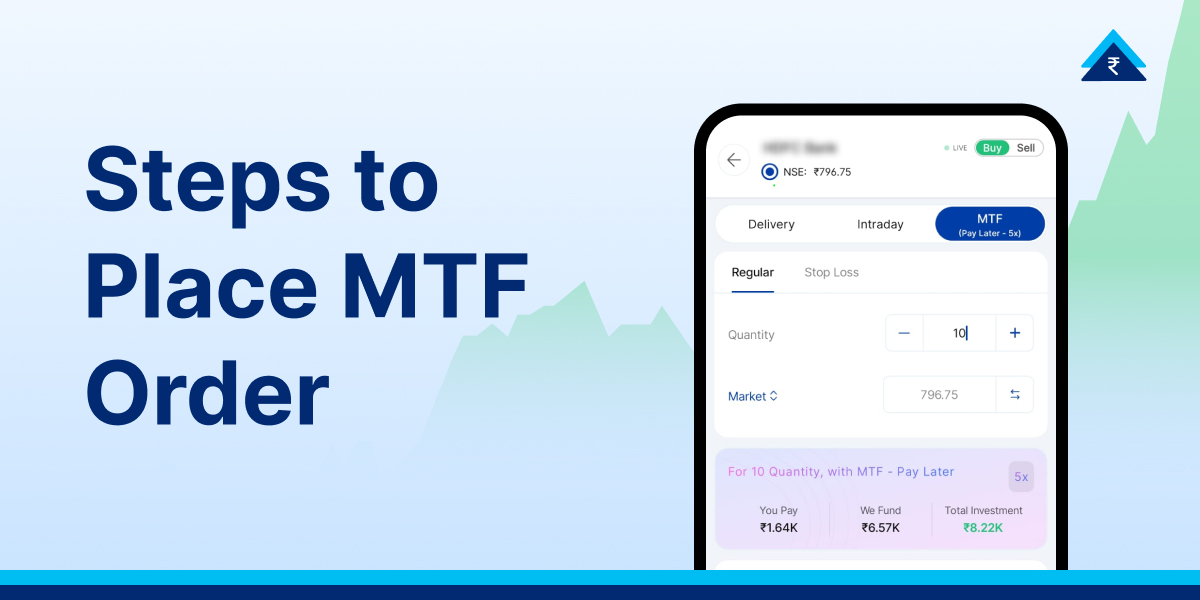

Method 1: Margin Trading Facility (MTF)

The most common and seamless way to buy stocks with borrowed money is through a Margin Trading Facility (MTF) provided directly by your stockbroker. When you activate MTF, your broker funds a significant portion of your stock purchase, while you pay only a fraction of the total cost upfront (the margin). For example, if a stock requires a 25% margin, you only need ₹25,000 to buy shares worth ₹100,000. The broker funds the remaining ₹75,000, and you pay an annualized interest rate on that borrowed amount. SEBI regulations allow authorized brokers to offer this facility, enhancing your buying power and allowing you to hold delivery positions (often up to T+365 days, depending on the broker) without paying the full amount immediately.

Margin Trading Facility (MTF): A formalised borrowing service provided by SEBI-authorised brokers allowing investors to buy stocks by paying only a fraction of the total transaction value.

Margin: The initial amount of money or collateral you must deposit with your broker to initiate a leveraged trade.

To use MTF, SEBI mandates that investors provide collateral. Previously, only cash was accepted, but under current SEBI guidelines, you can pledge the shares you already hold as collateral. Highly volatile stocks will require a higher margin, while stable blue-chip stocks will require a lower margin.

While industry interest rates typically range from 12% to 18% per annum, Paytm Money offers a highly competitive headliner rate of 7.99% p.a., significantly enhancing your buying power.

Method 2: Loan Against Securities (LAS)

If you already have a portfolio of stocks, mutual funds, or bonds, you can pledge them to a bank or NBFC to get a loan—this is called Loan Against Securities (LAS).

Unlike MTF, where the broker funds a specific stock purchase, LAS typically provides an overdraft facility in your bank account. You have the flexibility to use the funds for personal needs or to invest further in the stock market.

For equity shares, the Loan-to-Value (LTV) ratio is typically around 50%, in line with RBI guidelines for NBFCs, though this may vary by lender and asset type. This means if you pledge shares worth ₹10 Lakh, the maximum loan limit you will be granted is ₹5 Lakh.

The greatest benefit of LAS is that you do not have to sell your long-term investments (thus avoiding capital gains tax and retaining dividend rights), yet you get access to instant capital at interest rates that are usually lower than standard personal loans. However, since the loan is linked to market value, a fall in prices can lead to margin calls or liquidation of pledged securities.

Loan-to-Value (LTV) Ratio: A financial term used by lenders to express the ratio of a loan to the value of an asset purchased or pledged.

Method 3: Margin Pledge

If you do not want to take a formal cash loan like LAS or pay the daily interest rates associated with MTF, but still want to increase your trading capital, the Margin Pledge system is a highly efficient alternative. Through this method, you can pledge the existing stocks, Exchange Traded Funds (ETFs), Sovereign Gold Bonds (SGBs), or mutual funds sitting idle in your Demat account to your stockbroker. In return, the broker provides you with “collateral margin,” which essentially acts as increased buying power on your trading terminal. You can use this enhanced limit to take larger intraday equity positions, trade in Futures and Options (F&O), or fulfill the initial margin requirements for MTF trades.

The biggest advantage of a Margin Pledge is cost-efficiency. Unlike cash loans that charge a percentage-based interest rate, pledging securities usually only incurs a nominal, flat transaction fee (₹20/- per Transaction, plus GST on Paytm Money) charged by the depository.

Know more about Margin Pledge here.

Method 4: Personal Loans – Are They Allowed?

Many retail investors wonder if they can simply take a personal loan from a bank and funnel that money into their trading account. Technically, once a personal loan is disbursed into your savings account, it is fungible cash. However, practically and legally, taking a personal loan to invest in the stock market is a violation of the “end-use” terms set by the lender.

The RBI strictly monitors credit flow to the capital markets to prevent systemic risks. Most bank loan agreements explicitly state that the funds cannot be used for speculative activities, stock market investments, or buying cryptocurrency. If a bank discovers that a borrower has diverted personal loan funds into equity markets, they reserve the right to recall the entire loan immediately. Furthermore, personal loans carry exceptionally high interest rates (often 12% to 24%), which means your stock market returns must consistently beat this interest rate just to break even—an incredibly difficult feat even for seasoned professionals.

Pros and Cons of Buying Stocks with Borrowed Money

Before logging into your trading app and activating margin funding, it is crucial to weigh the advantages against the severe risks.

The Pros:

- Amplified Returns: Leverage allows you to buy more shares than your capital permits. If the stock price rises, your profits are calculated on the total number of shares, not just the fraction you paid for, supercharging your Return on Investment (ROI).

- No Need to Liquidate Portfolio: With facilities like LAS or pledging for MTF, you can capitalize on short-term market opportunities without disturbing your long-term wealth-creation portfolio.

- Dividend and Corporate Action Benefits: Even if your shares are pledged as collateral, you continue to receive dividends, bonuses, and rights issues on those stocks.

The Cons:

- Amplified Losses: Just as leverage magnifies profits, it brutally magnifies losses. If a stock falls, you not only lose your capital but you still owe the broker the borrowed amount plus interest.

- Margin Calls: If the value of your purchased stocks or pledged collateral drops below a required maintenance margin level due to market volatility, the broker or bank will issue a margin call. You will be forced to urgently deposit more cash or pledge more shares. Learn how to navigate MTF trades during market corrections.

- Forced Liquidation: If you fail to meet a margin call, the broker or lender has the legal right to sell your shares in the open market without your permission to recover their funds, turning a paper loss into a permanent one.

- Compounding Interest Burden: Borrowing isn’t free. The daily interest charged on MTF or LAS eats directly into your profits. In a sideways or stagnant market, you will lose money simply due to the cost of borrowing.

Margin Call: A demand by a broker that an investor deposit further cash or securities to cover possible or unrealised losses.

Forced Liquidation: The involuntary sale of an investor’s assets or positions by a broker to cover a margin shortfall.

Transparent Pricing Structure of Paytm Money

Paytm Money has designed preferential slabs to cater to retail investors and high-net-worth individuals alike. Even at the maximum tier of 9.99%, the rates remain incredibly competitive, ensuring that as your portfolio grows, your costs remain strictly controlled.

| Pay Later (MTF) Book Size | Interest Rate (p.a.) |

|---|---|

| Up to ₹1 Lakh | 7.99% |

| ₹1.01 Lakh – ₹1 Crore | 9.99% |

| Above ₹1 Crore | 8.99% |

Brokerage is charged at 0.1% of trade value or current brokerage, whichever is higher. Check Paytm Money Pricing.

Key Regulatory Guidelines to Remember

To ensure a safe trading environment, the regulators (SEBI and RBI) frequently update their guidelines. Here is a quick summary of the current framework governing borrowed investments in India:

- RBI’s LTV Cap: Banks and NBFCs cannot provide a loan exceeding 50% of the market value of pledged equity shares.

- SEBI’s Margin Pledge System: To prevent broker fraud, SEBI introduced a direct margin pledge system. Your shares never leave your Demat account; a lien is simply marked in favor of the broker or clearing corporation.

- Eligible Securities: Not all stocks can be bought on margin. SEBI pre-defines a list of liquid, fundamentally sound securities (usually Nifty 500 stocks and approved ETFs) eligible for MTF.

- Funding Limits: Under MTF, the maximum funding allowed by a broker is typically capped per client (e.g., ₹50 crore overall) and per stock to prevent concentrated risk.

Lien: A legal right or claim against a property (in this case, shares) by a creditor (broker/bank) to secure the repayment of a debt.

Clearing Corporation: An organization associated with an exchange that handles the confirmation, settlement, and delivery of transactions.

Conclusion

Buying stocks with borrowed money in India is absolutely possible and highly accessible through instruments like the Margin Trading Facility (MTF) and Loan Against Securities (LAS). However, it is a double-edged sword. While it offers the tantalizing prospect of amplified wealth, it exposes you to amplified risk and the relentless pressure of interest costs. Unsecured borrowing, like taking a personal loan for stock trading, is both regulatory non-compliant and financially hazardous. Before utilizing borrowed funds, investors must have a strict risk management framework, an iron-clad stop-loss strategy, and the financial capacity to absorb severe losses without derailing their personal finances.

Disclaimer: Investment in securities market is subject to market risks. Read all the related documents carefully before investing. This content is purely for information purpose only and in no way is to be considered as an advice or recommendation. The securities are quoted as an example and not as a recommendation. Investors are requested to do their own due diligence before investing.

SEBI Reg No.: Broking – INZ000240532, Research Analyst – INH000020086, Depository Participant – IN-DP-416-2019, Depository Participant Number: CDSL – 12088800, NSE (90165), BSE (6707), MCX (57525), NCDEX (1315), MSEI (85300).

Registered Office: 136, 1st Floor, Devika Tower, Nehru Place, Delhi – 110019.

For complete Disclaimers, visit https://www.paytmmoney.com.