Contents

Gold prices have rallied over 40% in the last one year. As the world was grappling with uncertainty surrounding the COVID-19 pandemic, demand for the asset class rose rapidly due to its perception as a safe haven. As you might be aware, gold has delivered more than 30% returns in the last 6 months alone! Are you thinking about the best way to get an exposure to gold? Through this article we would analyse the various means to invest into gold and help you choose the right investment vehicle. Also we give you a bonus tip on what percentage of your portfolio should be invested in gold. Let us take a look at the various options in front of you.

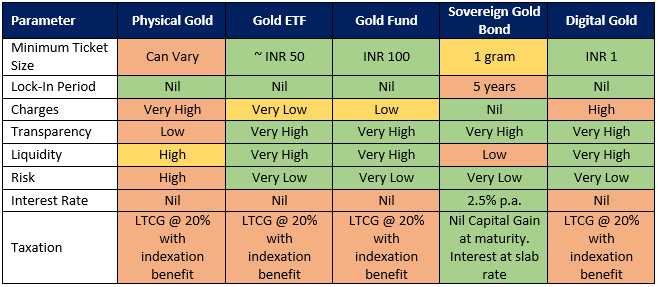

Physical Gold

One of the oldest way to own gold is to buy it physically from a nearby jewellery shop, bank or through online platforms. We Indians surely do love and cherish possessing gold. But keep in mind, that buying jewellery should not be construed as an investment. This is so because the making charges on jewellery can be as high as 25% in some cases plus GST which cannot be recovered on resale. Also owning physical gold has safety and storage concerns associated with it.

Gold ETF

It is an exchange traded fund with physical gold (99.5% purity) as the underlying asset. These ETFs are listed on an exchange like NSE or BSE where they can be bought or sold. The benefits of investing in gold ETFs primarily are transparency – price of a unit mimics the market price of gold closely at all times and liquidity – one can buy or sell the units anytime during market hours. The minimum investment that you can make is of 1 unit which starts around as low as INR 50. Additionally the capital gains tax treatment on these is similar to that of debt mutual funds i.e. taxed as per slab rate if held for less than 3 years and 20% with indexation benefits if held for more than 3 years.

ETFs surely are a cost effective way of buying gold relative to the physical route, however there are certain costs associated with it. It is mandatory to have a demat account in order to trade in Gold ETFs so an investor has to bear the cost of opening a demat account and brokerage charges on execution of the transaction. ETFs also have a cost associated with them which can range from 0.35% to 1.15%. Also, being an ETF, it is susceptible to tracking error which is the price difference between a unit and the actual price of gold. These are mere investment vehicles and you can in no way take physical delivery of gold by investing in Gold ETFs.

Gold Funds

These are mutual funds with a fund-of-fund (FoF) structure in general. These funds either have a Gold ETF as an underlying asset or a mutual fund which predominantly invests in shares of gold mining and related companies. The pros of investing in gold funds are that you can invest in these without having a demat account, low minimum ticket size – you can invest in them starting as low as INR 100 and it provides easy liquidity and transparency. The cons are that you end up paying a higher expense compared to an ETF and the FoFs having gold companies as underlying investment will also be susceptible to company specific risks. Also, physical delivery of gold is not possible through these funds. Finally, capital gains tax treatment is the same as Gold ETFs.

Sovereign Gold Bonds (SGBs)

Another interesting way to invest in gold is to buy SGBs offered by the RBI on behalf of the government. These are generally not available for subscription throughout the year. The RBI usually comes with a half yearly issuance calendar in advance. These bonds can be bought in multiples of gram(s) of gold. Thus, the minimum permissible investment is for 1 gram. The maximum subscription allowed in a fiscal year is up to 4 kg of gold. The purity of the underlying gold is 99.9% and you can get a discount of INR 50 per gram on online purchase. The biggest benefit of the SGB is that it provides an additional interest of 2.5% per annum on top of the appreciation in price of gold thus making it an attractive investment option. As the interest payments are semi-annual, these also provide you regular income.

The biggest drawback of these bonds are that they come with an 8 year tenure and a 5 year lock-in. Although SGBs are listed on exchanges and you can sell them in secondary market and exit, the liquidity is generally low in this case. Further these bonds are exempt from capital gains taxation at maturity which is a big relief. However, the interest earned is added to your income and taxed as per existing slab rate. Also, you do not have to incur any safety or storage risk. But physical delivery of gold is not possible.

Digital Gold

A new way of investing in gold which is catching on slowly is digital gold which is offered by Paytm in association with MMTC-PAMP (a GoI entity) and certain other platforms as well. The biggest benefit of buying digital gold is that you can buy it starting merely INR 1! The gold bought is 99.9% pure and is stored in highly secure vaults with MMTC-PAMP for which you pay zero storage costs. You can also redeem your investment when you feel like or take physical delivery of your accumulated gold in the form of a coin or bar. However, you need to bear certain making and transport charges which can eat into your returns. You can buy or sell digital gold anytime or day and the platform displays live gold prices for buying and selling as well.

To understand which product will be suitable for you let us compare the above offerings:

What should you invest in?

Your investment choice should be a function of your need. If you want to buy gold for a function like children’s marriage etc. then you should go with physical gold. But if you want to get an exposure to gold purely from an investment sense then Sovereign Gold Bond (SGB) should be your ideal choice. You stand to benefit from the extra 2.5% p.a. interest rate apart from the appreciation in gold prices while incurring zero charges and being exempt from capital gain taxation! The next issue of SGB opens from Aug 31st to 4th September.

Gold as an asset class provides you the benefit of diversification being a safe haven. Although it has given phenomenal returns in the recent past, it has also seen extended periods of poor performance in the past. It is advisable to invest only a small portion, up to 5-15% of your overall portfolio in gold depending on your risk profile.